Par Lisa Jacques & Paul Moltoni, étudiants ESTA Belfort, 05/2020

Mots-clés: #carbon pricing #carbon tax #emission trading scheme #Paris agreement #CO2 emissions

As a result of today’s challenges related to global warming, the first international agreement on climate and environment has been negotiated in Paris under the United Nations Framework Convention on Climate Change (UNFCCC). The main goal of this agreement is to keep the increase of the global temperature clearly below 2°C above pre-industrial revolution, and to keep on working on the already existing measures in order to prevent the global temperature to increase more than 1,5°C, as it will reduce risks and impacts related to global warming (UNFCCC, 2015). In order to achieve this target temperature, each country need to plan, act and report from its actions against climate change. Recognized by the Paris Agreement (2015) as an effective (if not mandatory) way of reducing carbon emissions, carbon pricing mechanisms have been either planned or, at least considered, by almost 100 countries in their Nationally Determined Contribution (NDC, which is basically the plan every country has to hand to the UNFCCC), as shown by the World Bank’s annual report “State and Trends of Carbon Pricing”, 2019. An important point to mention is that, besides being instrumental in the creation of international strategies such as the 1997 Kyoto Protocol or the Paris Agreement, the United States have shared their intention to withdraw from the Paris Agreement, and began the formal process of pulling out in late 2019, cutting short their commitment to prevent global warming as part of the United Nations (US Department of State, 2019). The aim of this article is to analyse what are the existing carbon pricing mechanisms, how efficient they actually are and their limits.

The main mechanisms of carbon pricing

To reduce greenhouse gas emissions, two carbon pricing instruments have been established for governments who ratify the Paris Agreement: emissions trading systems (ETS) and carbon taxes. Governments can choose one of the two instruments, or even both of them (State and Trends of Carbon Pricing, 2019)

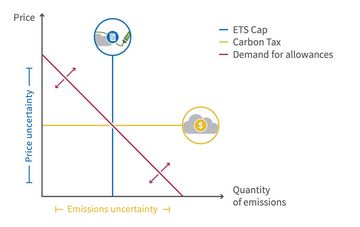

On the one hand, the ETS also known as a cap-and-trade system, operate according to the « cap and trade » principle: the government sets a cap on total emissions, and companies are required to hold one permits for every ton of emissions they produce; they can receive, buy or trade these permits, the value of which represents the price of carbon.

On the other hand, and according to youmatter.world website in 2020, “carbon taxes set a direct price on carbon as they establish a tax rate on greenhouse gases emissions. Contrary to the cap and trade system, with carbon taxes, the emission reduction outcome is not predefined. Furthermore, there are also other indirect ways to price carbon such as taxing fossil fuels or removing fossil fuel subsidies. Trade policies where tariffs on solar or wind-generated electricity are reduced, or renewable portfolio standards where the electric grid has to be a mix with a minimum share of clean energy, are also alternative ways of pushing carbon emissions out.”

By setting a cap, according to the ICAP, an ETS determines the total amount of emissions and ensures the outcome of mitigation measures. As a result, the price of carbon in each ETS depends on the demand for allowances. The price is likely to be higher in a prosperous economy and lower in a recession. In the case of the carbon tax, the price is predictable, but the outcome of mitigation measures cannot be guaranteed.

The taxes put in place reflect what citizens spend on insurance or ‘taxes’. Greenhouse gas emissions lead to climate change, cause extraordinary weather events such as hurricanes, frequent flooding or even rising sea levels leading to population migration, and increase the likelihood of medical problems such as cancer. Thus, these new taxes put in place reflect the expenses previously incurred by citizens through the taxes they pay or through insurance (health, housing, etc.). Thus, thanks to carbon taxation or ETS, the problem would be managed at source, sustainable energies would become as much, or even potentially more competitive from a financial point of view, and thus facilitate the transition to cleaner or renewable fuels. (Connect4Climate, 19/10/2016)

State of carbon pricing policies

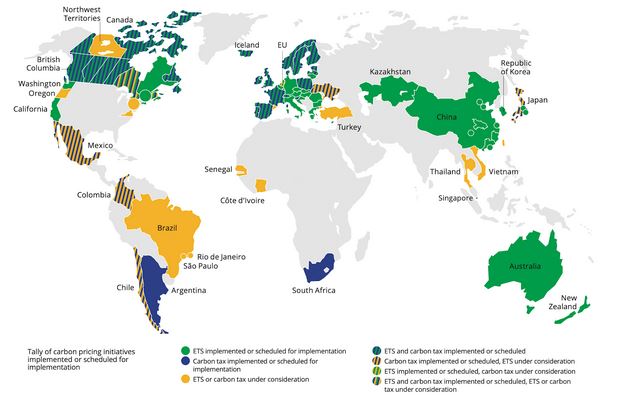

As shown by the World Bank in its annual report on the state of Carbon Pricing from 2019, the map below presents the current implementation of carbon pricing mechanisms (ETS or carbon tax, implemented, scheduled or under consideration for implementation).

This is a total of 57 implemented or scheduled initiatives for implementation, which covers 11 Gigatons of carbon dioxide equivalent, or 20% of the global greenhouse gases emissions.

The European Union decided in 2005 to implement an ETS, known as EU ETS, increased the covered Europe’s emissions from 40% to 52% in 2019 (Carbon Market Watch & World Bank, 2017 and 2019). The range price of one ton of CO2e was from US$1 to US$127, which is the highest price implemented by the Swedish government thanks to their carbon tax policy. The current issue with carbon pricing is that there is no floor price concerning the ETS implemented. This leads more than 50% of the emissions covered to be priced under US$10/tCO2e (State and Trends of Carbon Pricing, 2019). This price is unfortunately way below the floor price that we would need to implement, in order to reach the PA goals as set up by the UNFCCC. Indeed, the minimal price range should be between US$40 and US$80/tCO2e, so at least three times bigger than the current average of carbon pricing. An interesting point to mention is that France is currently meeting this goal with its carbon tax, as the government currently charge US$50 per tons of carbon dioxide equivalent. Carbon pricing policies also generated more than US$44 Billion revenue in 2018, that government reinvested or redistributed to their people. Other interesting fact: “the France carbon tax contributed to more than a third of global carbon tax revenue”, according to the World Bank annual report from 2019 (State and Trends of Carbon Pricing, 2019).

We will now take a closer look at the existing carbon pricing policies and their actual efficiency. British Columbia implemented a carbon tax in 2008, and it is now covering 72% of their CO2 emissions. As explained by the BC Prime Minister in an interview to the World Bank in 2015, the country decides to tax more what they do not want to see anymore (such as carbon emissions), and to tax less what they do want to see more (such as income, investments and wealth). This leads to a redistribution of the carbon tax generated revenues to the population, ending up to almost a quarter of their population not paying income taxes anymore. Of course, this carbon tax implementation is only made possible by redistribution and clear intentions from the government to cut taxes for individuals and small businesses for example, in order to show where the money comes from and where it is going to be used for.

Second interesting example about the carbon tax is Sweden. Thanks to a trusted government, tax reliefs for individuals and transparency, the tax was implemented in 1991 and lead by the end of 2017 to a decrease by 26% of their greenhouse gases emissions (Torbjörn Schiebe, 2019). Although very efficient in the reduction of emissions, it is important to mention that the reduction is mainly due to the production of fossil-free electricity and implementation of district heating networks.

Regarding the EU ETS for example, we can also see that despite low carbon price (around US$25/tCO2e in average), the implementation of the carbon market saved more than 1 billion tons of CO2e between 2008 and 2016, which is about 3.8% of emissions these years (Patrick Bayer and Michaël Aklin, 2020). In comparison, the emission decreased by 4.1% just between 2017 and 2018 within the EU ETS covered installations (Report on the functioning of the European carbon market, 2019).

Limits to the carbon pricing mechanisms

There are obviously limits to carbon pricing mechanisms. Firstly, concerning the carbon tax system and as said before, the implementation of such a policy needs to be done accordingly to a well prepared, transparent and fair plan. As mentioned by Franziska Funke and Linus Mattauch in 2018, countries with efficient carbon tax policies are often linked with high political trust and low corruption level. When people do not know what the revenue generated by the tax is used for, or when it creates discrepancies between urban and countryside people for example because of a non-reinvestment of the revenues, they are obviously less likely to agree to such measures. This could be part of an explanation to why the increased in the French carbon tax led to such a social protest from the “yellow jackets”. Now let’s assume that the carbon tax is implemented and efficiently helps to decrease the CO2 emissions, as it actually is the case in Sweden. When reduction in the emissions becomes even greater, carbon tax generated revenues are going to shrink undeniably, leading to another dilemma concerning how to compensate with this loss in financial revenue in order to keep people’s well-being.

Secondly, there are limits to the emission trading systems. First issue is that there is usually a surplus of allowances in the ETS, leading to a lower price of carbon and therefore, a less efficient carbon market. There are already a few solutions to that problem: the governments could have more ambition for CO2 emission reduction and as a result, reduce the number of allowances, or the Market Stability Reserve of each ETS should absorb the surplus of allowances to ensure a sufficient number, or governments could consider to implementing a floor price for carbon, to ensure the needed level of carbon price to meet PA’s targets (Wijnand Stoefs, 2020). Another limit to the ETS is carbon leakage, which is basically when companies decide to outsource production to other countries, where carbon laws are less restrictive, although there is still no proof yet that this is happening within the EU ETS (Carbon Market Watch, 2019). Finally, one big issue related to carbon markets is the tax fraud it can generate. Obviously, the best example of this is the missing trader fraud (VAT fraud) which happened between 2008 and 2009, and which, according to the French Court of Audit in 2012, cost about 1,6 B€ to the French government, and more than 5 B€ to the EU-ETS members.

Regarding the current situation due to the global health crisis, we thought it would be interesting to analyze some of the impacts that the pandemic has on the EU carbon market. Since December 2019, the carbon price has been pretty stable, fluctuating more or less about €2 around €24/tCO2e. However, as any other financial market, the EU ETS collapsed during March 2020, leading to a carbon price falling within one week to €15/tCO2e on March 18th (Sam Van den Plas, 2020 and Ember Climate, 2020). The lower carbon price compulsory induces a revenue drop for state members and will help offset the economic loss of particularly polluting sectors such as the steel or chemical industries. The only way to stop the carbon price to drop further is to cancel the surplus of allowance as mentioned before, but the EU ETS Market Stability Reserve is somehow limited and governments are not currently focusing on the environment problem first, having other issues to deal with. The price is now somehow stabilizing around €20/tCO2e; however, we cannot take it for granted. The problem is that focusing on the classical economic point of view by helping industries and polluters first is not going to help us reach the PA’s goals, neither going through this environmental crisis.

As a conclusion to this article, we could say that the goals from the Paris Agreement are only achievable under the current situation of carbon pricing if the government of the most polluting countries decide to take serious measures in the very short run. We would like to mention that, according to Linus Mattauch and other researchers, always linking decarbonization of the society and economic growth is probably a misleading. As per their study’s results, the most CO2 emitting sectors are not the ones that bring the biggest amount of value-added growth. This basically shows that even though governments are taxing more those industries, the economy would not shrink as an inevitable result, as those sectors are not the ones that affect prosperity in a larger scale. Therefore, increasing the installations covered by the ETS worldwide and implementing a floor price to carbon which matches the Paris Agreement requirements (between US 40-80$/tCO2e for 2020) look like viable and feasible measures.

Références

Bayer P. and Aklin M., 2020, “The European Union Emissions Trading System reduced CO2 emissions despite low prices”, Proceedings of the National Academy of Science, first published April 6, 2020, [viewed 28/04/2020]. Available from: The European Union Emissions Trading System reduced CO2 emissions despite low prices

Carbon Market Watch, “EU carbon market”, [viewed 28/04/2020]. Available from: EU carbon market

“Carbon Pricing And Carbon Credits: Definition, Examples and History”, You Matter, last modified on 2020, March 21th, [viewed 28/04/2020] Available from: Carbon Pricing And Carbon Credits: Definition, Examples And History

Clark C., 2015, “Premier: Tax carbon, cut taxes on income and business for a more competitive environment”, World Bank,[viewed 28/04/2020]. Available from: Premier: Tax carbon, cut taxes on income and business for a more competitive environment

Commission to the european parliament, 2019, “Report on the functioning of the European carbon market”, [viewed 28/04/2020]. Available from: 52019DC0557R(01) – EN – EUR-Lex

Connect4Climate, (19/10/2016). Climate Countdown: Carbon Pricing – #Film4Climate « Price On Carbon Pollution » Award Winner. YouTube. [28/04/2020]. Available from: https://www.youtube.com/watch?v=NA59sLmtIFE&feature=emb_logo&fbclid=IwAR0wxNF_yRCxxQYiozia4lkTEv2mtcTXr7BjHUy9HtkILcCzfzl0H3IF9hk

Cour des comptes, 2012, “Rapport public annuel 2012 – février 2012”, [viewed 28/04/2020]. Available from: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&ved=2ahUKEwiJ9bGehozpAhWJsBQKHSqNA4wQFjAAegQIAhAB&url=https%3A%2F%2Fwww.ccomptes.fr%2Fsites%2Fdefault%2Ffiles%2FEzPublish%2FFraude_TVA_sur_quotas_carbone.pdf&usg=AOvVaw1BD-WqvcJy5F7S6QWUKQHT

Discrepancy between carbon tax and ETS, from International Carbon Action Partnership, Published on 8 April 2019 : Emissions Trading and Carbon Tax: Two Instruments, One Goal (figure 1) https://icapcarbonaction.com/en/?option=com_attach&task=download&id=638

Ember-Climate, Carbon Price Viewer, [viewed 10/05/2020]. Available from: Carbon Price Viewer

Funke F. and Mattauch L., 2018, “Why is carbon pricing in some countries more successful than in others?”, Our World in Data, [viewed 28/04/2020]. Available from: Why is carbon pricing in some countries more successful than in others?

Mattauch L., Radebach A., Siegmeier J., and Sulikova S., “Shrink emissions, not the economy!”, Our World in Data, [viewed 28/04/2020]. Available from: Shrink emissions, not the economy!

Nations Unies, 2015, Paris Agreement. Available from: Paris Agreement

Pompeo M.R. , 2019, “On the U.S. Withdrawal from the Paris Agreement”, U.S Department of State, [viewed 28/04/2020]. Available from: On the US Withdrawal from the Paris Agreement

Schiebe T., 2019, “Should every country on earth copy Sweden’s carbon tax?”, Carbon Pricing Leadership Coalition, [viewed 28/04/2020]. Available from: Should every country on earth copy Sweden’s carbon tax? — Carbon Pricing Leadership Coalition

“State and Trends of Carbon Pricing 2019” State and Trends of Carbon Pricing (June), World Bank, Washington, DC. Available from : State and Trends of Carbon Pricing 2019

Stoefs W., 2020, “EU carbon market state aid rules moving in the right direction – but not far enough”, Carbon Market Watch, [viewed 28/04/2020]. Available from: EU carbon market state aid rules moving in the right direction – but not far enough

Summary map of regional, national and subnational carbon pricing initiatives implemented, scheduled for implementation and under consideration (ETS and carbon tax), “State and Trends of Carbon Pricing 2019”, World Bank (figure 2)

The Paris Agreement, 2019, “The Paris Agreement”, UNFCCC, [viewed 28/04/2020]. Available from: Paris Climate Change Agreement

Van Den Plas S., 2020, “When COVID-19 met the EU ETS”, Carbon Market Watch, [viewed 28/04/2020]. Available from: When COVID-19 met the EU ETS

Really informative article !

This subject can be complex, but it was well explained. It was easy to follow and to know what the purpose of this article is. I also really liked the way you compared both methods and explained the advantages as well as disadvantages. The images and the video supported this article really well to understand the methods even more. I can tell you put a lot of effort into the video !

Good job ! 🙂

J’aimeJ’aime